Credit Card Utilization Penalty Points Are Charged Once Balance Exceeds

Onlines

Apr 03, 2025 · 6 min read

Table of Contents

Credit Card Utilization Penalty Points: When Your Balance Goes Over the Limit

Credit cards offer convenience and financial flexibility, but exceeding your credit limit can lead to significant penalties, impacting your credit score and overall financial health. Understanding how credit utilization impacts your credit score and how to avoid those pesky penalty points is crucial for responsible credit card management. This comprehensive guide delves into the mechanics of credit utilization, explores the consequences of exceeding your credit limit, and offers practical strategies for maintaining a healthy credit utilization ratio.

Understanding Credit Utilization and its Impact on Your Credit Score

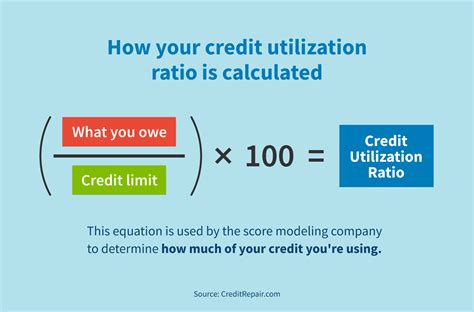

Credit utilization refers to the ratio of your outstanding credit card balance to your total available credit. Lenders closely monitor this ratio as it's a key indicator of your creditworthiness. A high credit utilization ratio suggests you're heavily reliant on credit and may struggle to manage your finances effectively. Conversely, a low credit utilization ratio signals responsible credit management and a lower risk to lenders.

How Credit Utilization Affects Your Credit Score:

Credit scoring models, such as FICO and VantageScore, consider credit utilization as a significant factor. A high credit utilization ratio can negatively impact your credit score in several ways:

-

Increased Risk Perception: Lenders perceive a high utilization ratio as a higher risk of default. If you're consistently using a large portion of your available credit, it signals you may be overextending yourself financially.

-

Lower Credit Limit Increase Approvals: Maintaining a low utilization ratio makes you a more attractive borrower. Lenders are more likely to approve credit limit increases for individuals who demonstrate responsible credit management.

-

Higher Interest Rates: Lenders often charge higher interest rates to borrowers with high credit utilization ratios because they represent a higher risk.

-

Penalty Fees: Many credit card issuers impose penalty fees when you exceed your credit limit. These fees can significantly impact your overall financial health.

The Crucial Role of Penalty Points

While not explicitly referred to as "penalty points" by credit bureaus, exceeding your credit limit leads to consequences that negatively impact your credit score, effectively acting as penalty points. These consequences include:

-

Negative Reporting to Credit Bureaus: Exceeding your credit limit is often reported to the credit bureaus as a negative item, directly impacting your credit score. The severity of the negative impact depends on the extent and duration of the over-limit situation.

-

Increased Interest Rates: Many credit card companies will immediately raise your interest rate as a penalty for exceeding the limit. This increased interest rate applies to your existing balance and all future purchases, adding further financial strain.

-

Late Payment Fees: Even if you pay your balance in full, exceeding your credit limit could trigger late payment fees if the payment is processed after the billing cycle. This is because some companies calculate late payments based on the actual payment date, not the due date.

What constitutes "exceeding the credit limit"?

It's crucial to understand that even going slightly over your limit can trigger these negative consequences. There is no grace period that usually applies to exceeding your credit limit, as opposed to late payments where sometimes there is. Avoid the problem altogether.

Avoiding Credit Card Utilization Penalty Points: Practical Strategies

Maintaining a healthy credit utilization ratio is crucial for protecting your credit score and avoiding penalty points. Here are several effective strategies to ensure you stay within your credit limits:

1. Monitor Your Spending Closely:

Regularly track your spending habits using budgeting apps, spreadsheets, or even a simple notebook. Knowing where your money goes is the first step to controlling it. Be mindful of recurring expenses and upcoming large purchases.

2. Set Spending Limits and Stick to Them:

Before swiping your credit card, consider whether the purchase aligns with your budget. Setting realistic spending limits for each month prevents overspending and exceeding your credit limit.

3. Pay Your Bills on Time, Every Time:

Always strive to pay your credit card balances in full and on time. This demonstrates responsible credit management and prevents late payment fees and negative impacts on your credit score. This reduces the utilization ratio.

4. Increase Your Credit Limit (If Necessary and Responsible):

If you consistently use a large portion of your available credit, consider requesting a credit limit increase from your credit card issuer. This will lower your credit utilization ratio, but only if you keep spending at the same level. Don't increase the spending!

5. Utilize Multiple Credit Cards Wisely:

Diversifying your credit across multiple cards can help lower your overall credit utilization. Use each card strategically and keep track of balances and payments across all cards.

6. Regularly Review Your Credit Report:

Obtain your free credit reports annually from each of the three major credit bureaus (Equifax, Experian, and TransUnion). Review your reports for any discrepancies or errors related to credit utilization.

7. Pay Down Debt Aggressively:

If you have a high credit utilization ratio, prioritize paying down your credit card debt as quickly as possible. Consider debt consolidation options or balance transfers to reduce your interest payments and lower your utilization ratio more quickly.

8. Avoid Cash Advances:

Cash advances often come with high fees and interest rates. These charges can quickly increase your credit card balance and negatively impact your credit utilization ratio.

9. Understand Your Credit Card Agreement:

Carefully review the terms and conditions of your credit card agreement, paying close attention to the clauses related to credit limits, penalties, and interest rates.

10. Contact Your Credit Card Issuer:

If you're experiencing financial difficulties or anticipate exceeding your credit limit, contact your credit card issuer immediately. They may offer solutions to help you avoid penalty fees or other negative consequences.

The Long-Term Impact of Exceeding Your Credit Limit

The consequences of exceeding your credit limit are not limited to immediate penalties. The negative impact can extend for years, affecting your ability to obtain loans, mortgages, and even insurance at favorable rates. A damaged credit score makes borrowing more expensive and challenging in the long run.

Long-term financial implications include:

-

Higher Interest Rates on Loans: Lenders often assess higher interest rates on loans, like auto loans and mortgages, based on your credit score. This increases the overall cost of borrowing.

-

Difficulty Getting Approved for Loans: A low credit score due to exceeding credit limits may make it more difficult to get approved for loans or credit lines. Lenders consider your credit score a key indicator of risk.

-

Rejected Rental Applications: Some landlords and property management companies check your credit report when evaluating rental applications. A low credit score due to credit utilization issues may result in rental application rejections.

-

Higher Insurance Premiums: Insurance companies often use credit scores to assess risk. A low credit score can result in higher premiums for auto, home, or renter's insurance.

-

Employment Challenges: While less common, some employers may perform credit checks during the hiring process. A low credit score can negatively impact your employment prospects.

Conclusion: Responsible Credit Card Management is Key

Avoiding credit card utilization penalty points requires diligent planning, consistent monitoring, and a commitment to responsible credit management. By following these strategies, you can significantly improve your chances of maintaining a healthy credit utilization ratio, protecting your credit score, and ensuring long-term financial well-being. Remember, your credit score is a valuable asset. Treat it with respect and care. Proactive credit management is significantly cheaper and easier than repairing a damaged credit history later on.

Latest Posts

Latest Posts

-

Which Of The Following Is The Best Example Of Cogeneration

Apr 04, 2025

-

What Are Two More Purposes Of The Violent Incident Log

Apr 04, 2025

-

Kumon Answer Book Pdf Level D

Apr 04, 2025

-

Select The Social Media Site That Is An Idea Sharing Website

Apr 04, 2025

-

7 7 Skills Practice Scale Drawings And Models

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about Credit Card Utilization Penalty Points Are Charged Once Balance Exceeds . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.