Which Of The Statements Below Explains The Accounting Cycle

Onlines

Mar 28, 2025 · 8 min read

Table of Contents

Which of the following statements explains the accounting cycle? Understanding the Flow of Financial Information

The accounting cycle is the backbone of any business's financial health. It's a systematic process that ensures accurate and timely recording of financial transactions, culminating in the creation of financial statements. Understanding this cycle is crucial, not just for accountants, but for anyone involved in managing a business, from entrepreneurs to investors. This article will delve deep into the accounting cycle, exploring its various stages and clarifying what constitutes a complete and accurate representation of this vital process. We will also analyze common misconceptions and provide a clear, concise explanation to address the question: which statement best explains the accounting cycle?

Understanding the Core Components of the Accounting Cycle

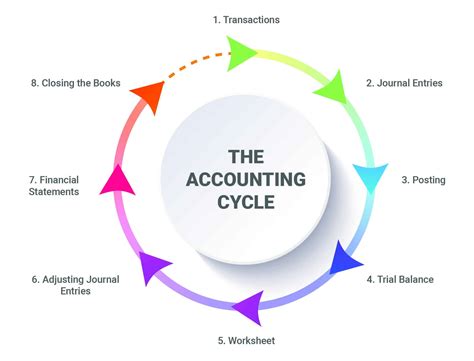

Before we examine statements describing the accounting cycle, let's establish a firm understanding of its core components. The cycle is a continuous loop, but we can break it down into key stages for easier comprehension:

1. Identifying and Analyzing Transactions

This initial stage involves meticulously identifying all financial transactions that affect the business. This could range from sales and purchases to receiving payments and incurring expenses. The crucial next step is analyzing each transaction to determine its impact on the accounting equation (Assets = Liabilities + Equity). Each transaction will affect at least two accounts. For example, a purchase of inventory on credit will increase inventory (an asset) and increase accounts payable (a liability). Accurate analysis is paramount for preventing errors that can cascade through the entire cycle.

2. Journalizing Transactions

Once transactions are analyzed, they're recorded in a journal. The journal is a chronological record of each transaction, using a standardized format called a journal entry. Each journal entry includes the date of the transaction, accounts affected, the debit and credit amounts, and a brief description. Debits and credits are fundamental to double-entry bookkeeping; debits increase assets and expenses, while credits increase liabilities and equity. Maintaining a meticulous journal is key to creating an accurate record of all financial activities.

3. Posting to the Ledger

The next step involves transferring information from the journal to the ledger. The ledger is a collection of individual accounts, each tracking a specific element of the business’s finances (e.g., cash, accounts receivable, inventory, etc.). This process, called posting, summarizes the transactions affecting each account, providing a detailed balance for each at any given time. The ledger serves as a central repository of all account balances, enabling easy access to individual account information. Regular reconciliation between the journal and ledger is essential to ensure data integrity.

4. Preparing a Trial Balance

A trial balance is a summary of all the ledger account balances at a specific point in time. It's used to verify that the debits equal the credits—a fundamental principle of double-entry bookkeeping. If the debits and credits don't match, it indicates an error in the journal entries or posting process, requiring careful review and correction. The trial balance doesn't guarantee the accuracy of the financial statements, but it serves as a crucial checkpoint before proceeding to the next stages.

5. Preparing Adjusting Entries

Adjusting entries are crucial for ensuring the financial statements accurately reflect the financial position of the business. These entries account for items not yet recorded but relevant to the accounting period. Common examples include adjusting for accrued expenses (like salaries payable), prepaid expenses (like insurance), unearned revenue, and bad debts. These entries are vital for the accurate reflection of revenues and expenses within the given accounting period, ensuring compliance with the accrual basis of accounting.

6. Preparing Adjusted Trial Balance

After making adjusting entries, another trial balance is prepared – the adjusted trial balance. This reflects the account balances after incorporating the adjusting entries. This step serves as a final check for mathematical accuracy before the preparation of financial statements. This trial balance provides a foundation for creating accurate financial statements that provide a true and fair view of the business's financial performance.

7. Preparing Financial Statements

The culmination of the accounting cycle is the preparation of financial statements. These statements provide a summary of the business’s financial performance and position. They typically include:

- Income Statement: Shows the revenues, expenses, and net income or loss for a specific period.

- Balance Sheet: Shows the assets, liabilities, and equity at a specific point in time.

- Statement of Cash Flows: Shows the inflows and outflows of cash during a specific period.

- Statement of Changes in Equity: Shows the changes in the owner's equity during a specific period.

These statements provide critical insights into the business's financial health, enabling informed decision-making by management, investors, and creditors.

8. Closing the Books

The closing process involves transferring the balances of temporary accounts (revenue, expense, and dividend accounts) to the retained earnings account. This process resets these temporary accounts to zero, preparing them for the next accounting period. The closing entries formally end one accounting period and initiate the next, ensuring a clean start for the new cycle. This ensures the accuracy and clarity of financial reporting across different periods.

9. Preparing Post-Closing Trial Balance

Finally, a post-closing trial balance is prepared to verify that only permanent accounts (assets, liabilities, and equity) have balances after the closing entries. This serves as a final check to confirm the accuracy of the closing process before starting the next accounting cycle.

Analyzing Statements Describing the Accounting Cycle

Now let's consider potential statements describing the accounting cycle and determine which most accurately reflects the process. Many statements might partially describe the cycle, but a comprehensive statement must capture the entire flow from transaction identification to the final post-closing trial balance. A statement that solely focuses on journalizing or preparing financial statements would be incomplete.

Here are examples of statements that might be presented, along with an analysis of their accuracy:

Statement A: The accounting cycle involves recording transactions in a journal, posting to the ledger, and preparing financial statements.

Analysis: This statement is partially accurate. It includes some key steps but omits crucial aspects like adjusting entries, preparing trial balances, and closing the books. Therefore, it's an incomplete description.

Statement B: The accounting cycle is a continuous process that begins with identifying and analyzing transactions and ends with preparing financial statements.

Analysis: This statement is more accurate than Statement A. It includes the beginning and end points, but again lacks detail regarding crucial intermediate steps such as adjusting entries, trial balances, and the closing process. It is a better representation than Statement A, but still incomplete.

Statement C: The accounting cycle is a systematic process of identifying, recording, classifying, summarizing, and reporting business transactions to produce meaningful financial statements. This process encompasses journalizing, posting, preparing trial balances (both unadjusted and adjusted), making adjusting entries, and closing entries.

Analysis: Statement C offers a much more complete picture of the accounting cycle. It encompasses all the essential steps, from transaction identification to closing entries, and explicitly mentions the preparation of both unadjusted and adjusted trial balances. It clearly highlights the systematic nature of the process and the ultimate goal—producing meaningful financial statements.

Statement D: The accounting cycle involves summarizing all transactions in a general ledger and creating an income statement.

Analysis: This statement is far too limited. It only mentions two components (general ledger and income statement) and completely ignores the extensive processes involved in preparing and analyzing transactions, making adjusting entries and closing entries.

Conclusion: Of the statements provided, Statement C offers the most comprehensive and accurate explanation of the accounting cycle. It accurately encompasses all the key stages and emphasizes the systematic and iterative nature of the process.

The Importance of Accuracy in the Accounting Cycle

The accuracy of the accounting cycle is paramount for a variety of reasons:

-

Reliable Financial Reporting: Accurate financial statements are crucial for making informed business decisions. Inaccurate information can lead to poor management decisions, resulting in financial losses.

-

Compliance with Regulations: Accurate accounting is essential for complying with relevant accounting standards and regulations. Non-compliance can result in penalties and legal issues.

-

Investor Confidence: Investors rely on the accuracy of financial statements to assess the financial health of a company. Inaccurate reporting can damage investor confidence and lead to a loss of investment.

-

Lender Trust: Lenders use financial statements to assess the creditworthiness of a borrower. Accurate accounting is crucial for securing loans and maintaining a positive relationship with lenders.

-

Internal Control: A well-functioning accounting cycle contributes to a robust internal control system, which helps to safeguard assets, prevent fraud, and ensure operational efficiency.

Addressing Common Misconceptions

Several misconceptions surround the accounting cycle. It's crucial to address these to fully grasp the process:

-

Myth 1: The accounting cycle only involves preparing financial statements. The truth is that the preparation of financial statements is only the culmination of a far more extensive process.

-

Myth 2: The accounting cycle is only relevant to large corporations. The truth is that businesses of all sizes, from sole proprietorships to large multinational corporations, benefit from a well-functioning accounting cycle.

-

Myth 3: Technology has made the accounting cycle obsolete. While technology streamlines many aspects of the process, the underlying principles of the accounting cycle remain vital for financial reporting.

In conclusion, understanding the accounting cycle is vital for the financial health and success of any business. A complete and accurate understanding of this process ensures the generation of reliable financial statements, fosters investor and lender trust, and contributes to overall business efficiency and compliance. Statement C, which highlights the systematic nature of the process and includes all key stages, provides the most comprehensive explanation of the accounting cycle.

Latest Posts

Latest Posts

-

Which Sentence Best Paraphrases The Passage

Mar 31, 2025

-

5 1 8 Configure Network Security Appliance Access

Mar 31, 2025

-

Based On Your Observations Compare Typical Cervical

Mar 31, 2025

-

What Plate Do Residents Of Tallahassee Florida Live On

Mar 31, 2025

-

Funding 401k And Roth Ira Worksheet

Mar 31, 2025

Related Post

Thank you for visiting our website which covers about Which Of The Statements Below Explains The Accounting Cycle . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.