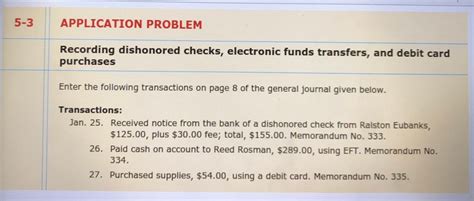

5 3 Application Problem Accounting Answers

Onlines

Apr 05, 2025 · 6 min read

Table of Contents

5-3 Application Problems: Accounting Answers and Solutions

This comprehensive guide delves into five common application problems encountered in accounting, providing detailed solutions and explanations. Understanding these problems is crucial for mastering fundamental accounting principles and building a strong foundation for more advanced concepts. We'll cover a range of topics, ensuring you grasp the underlying logic and can confidently tackle similar problems in your studies or professional work. Remember, accuracy and attention to detail are paramount in accounting.

Problem 1: Journal Entries and Trial Balance

Scenario: ABC Company completed the following transactions during its first month of operations:

- July 1: Invested $50,000 cash in the business.

- July 5: Purchased office equipment for $10,000 cash.

- July 10: Purchased supplies on account for $2,000.

- July 15: Received $5,000 cash for services performed.

- July 20: Paid $1,000 cash for rent expense.

- July 25: Paid $1,500 cash for salaries expense.

- July 30: Paid $1,000 cash on account.

Required: Prepare journal entries for each transaction and prepare a trial balance.

Solution:

First, let's create the journal entries:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| July 1 | Cash | $50,000 | |

| Owner's Equity (Capital) | $50,000 | ||

| To record investment of cash | |||

| July 5 | Office Equipment | $10,000 | |

| Cash | $10,000 | ||

| To record purchase of equipment | |||

| July 10 | Supplies | $2,000 | |

| Accounts Payable | $2,000 | ||

| To record purchase of supplies | |||

| July 15 | Cash | $5,000 | |

| Service Revenue | $5,000 | ||

| To record cash received for services | |||

| July 20 | Rent Expense | $1,000 | |

| Cash | $1,000 | ||

| To record rent expense | |||

| July 25 | Salaries Expense | $1,500 | |

| Cash | $1,500 | ||

| To record salaries expense | |||

| July 30 | Accounts Payable | $1,000 | |

| Cash | $1,000 | ||

| To record cash payment on account |

Next, we prepare the Trial Balance:

ABC Company Trial Balance July 31, 20XX

| Account Name | Debit | Credit |

|---|---|---|

| Cash | $42,500 | |

| Office Equipment | $10,000 | |

| Supplies | $2,000 | |

| Accounts Payable | $1,000 | |

| Owner's Equity (Capital) | $50,000 | |

| Service Revenue | $5,000 | |

| Rent Expense | $1,000 | |

| Salaries Expense | $1,500 | |

| Total | $57,000 | $57,000 |

Key takeaway: A trial balance ensures the debits and credits are equal, indicating a potential accuracy in the recording of transactions. Discrepancies necessitate review and correction of the journal entries.

Problem 2: Adjusting Entries

Scenario: At the end of the accounting period, ABC Company needs to make the following adjustments:

- Supplies Used: $500 worth of supplies were used during the month.

- Depreciation: Office equipment depreciates $100 per month.

- Accrued Salaries: $500 of salaries are owed to employees but haven't been paid.

Required: Prepare adjusting entries for each item.

Solution:

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| July 31 | Supplies Expense | $500 | |

| Supplies | $500 | ||

| To record supplies used | |||

| July 31 | Depreciation Expense | $100 | |

| Accumulated Depreciation - Office Equipment | $100 | ||

| To record depreciation | |||

| July 31 | Salaries Expense | $500 | |

| Salaries Payable | $500 | ||

| To record accrued salaries |

Key takeaway: Adjusting entries are crucial for accurately reflecting the financial position of a business at the end of an accounting period. They ensure that revenues and expenses are recognized in the proper period.

Problem 3: Accrual vs. Cash Accounting

Scenario: XYZ Company performed services for a client on December 28th, 20XX, but received payment on January 5th, 20XY. How would this transaction be recorded under accrual accounting and cash accounting?

Solution:

Accrual Accounting: Under accrual accounting, revenue is recognized when earned, regardless of when cash is received. Therefore, XYZ Company would record the revenue in December 20XX, even though they didn't receive payment until January 20XY.

Journal Entry (Accrual):

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| December 28 | Accounts Receivable | $XXX | |

| Service Revenue | $XXX | ||

| To record service revenue |

Journal Entry (Cash):

| Date | Account Name | Debit | Credit |

|---|---|---|---|

| January 5 | Cash | $XXX | |

| Accounts Receivable | $XXX | ||

| To record cash receipt |

Cash Accounting: Under cash accounting, revenue is recorded only when cash is received. Therefore, XYZ Company would record the revenue in January 20XY.

Key takeaway: The choice between accrual and cash accounting significantly impacts the timing of revenue and expense recognition. Accrual accounting provides a more accurate picture of a company's financial performance over time.

Problem 4: Bank Reconciliation

Scenario: The bank statement shows a balance of $10,000. The company's cash book shows a balance of $12,000. Outstanding checks total $1,500. A deposit in transit is $2,000. Bank charges are $50. A note receivable of $1,000 was collected by the bank.

Required: Prepare a bank reconciliation.

Solution:

Bank Reconciliation

ABC Company As of [Date]

Bank Statement Balance: $10,000

Add: Deposit in transit $2,000 Less: Outstanding checks $1,500 Adjusted Bank Balance: $10,500

Company's Cash Book Balance: $12,000

Less: Bank Charges $50 Add: Note receivable collected $1,000 Adjusted Book Balance: $12,450

Difference: $1,950

Possible reasons for discrepancy: There may be errors in either the bank statement or the company's cash book. A detailed investigation is necessary to identify the source of the discrepancy.

Key takeaway: Bank reconciliations are essential for verifying the accuracy of cash balances. This process highlights discrepancies that might otherwise go unnoticed, helping prevent fraud and ensure accurate financial reporting.

Problem 5: Inventory Valuation

Scenario: DEF Company uses the periodic inventory system. Beginning inventory was $10,000. Purchases during the period totaled $20,000. Ending inventory is $5,000. Calculate the cost of goods sold.

Solution:

Cost of Goods Sold (COGS) Calculation:

Beginning Inventory: $10,000

- Purchases: $20,000

- Ending Inventory: $5,000 = Cost of Goods Sold: $25,000

Key takeaway: Understanding different inventory valuation methods (like FIFO, LIFO, and weighted-average cost) is critical for accurate cost of goods sold calculations and ultimately impacts the reported net income. The periodic system relies on physical counts to determine the ending inventory.

This guide covers five crucial application problems in accounting. Mastering these concepts will significantly enhance your understanding and ability to tackle more complex accounting scenarios. Remember to always double-check your work and consult your accounting textbooks and resources for further clarification. Accurate accounting is essential for the financial health of any business.

Latest Posts

Latest Posts

-

Which Is A True Statement Regarding Gastric Cancer

Apr 06, 2025

-

Shadow Health Respiratory Assessment Answers Pdf

Apr 06, 2025

-

How Is Asymmetrical Balance Achieved In The Painting Below

Apr 06, 2025

-

Summary Of Act 3 Scene 2

Apr 06, 2025

-

Blood At The Root Dominique Morisseau Pdf

Apr 06, 2025

Related Post

Thank you for visiting our website which covers about 5 3 Application Problem Accounting Answers . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.