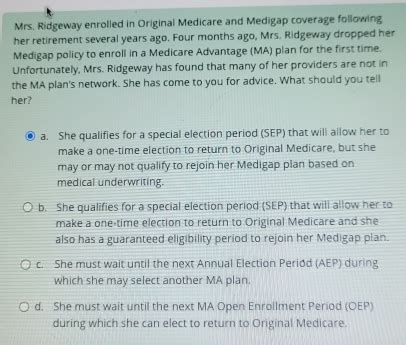

Mrs Ridgeway Enrolled In Original Medicare

Onlines

Mar 13, 2025 · 6 min read

Table of Contents

Mrs. Ridgeway Enrolled in Original Medicare: A Comprehensive Guide

Understanding Medicare can be a daunting task, especially for those newly eligible. This article delves into the specifics of Mrs. Ridgeway's enrollment in Original Medicare, exploring the intricacies of Parts A and B, potential supplemental coverage options (Medigap), and the importance of understanding her benefits and limitations. We will also address common questions and concerns surrounding Original Medicare enrollment.

Understanding Original Medicare: Parts A & B

Original Medicare, also known as traditional Medicare, comprises two main parts: Part A (hospital insurance) and Part B (medical insurance). These parts work together to provide comprehensive coverage, but they function differently and require understanding their respective roles.

Part A: Hospital Insurance

Mrs. Ridgeway's Part A coverage likely covers a significant portion of her hospital expenses. This includes inpatient hospital care, skilled nursing facility care, hospice care, and some home healthcare. Most individuals are eligible for premium-free Part A based on their work history and contributions to Social Security. However, it’s crucial to verify Mrs. Ridgeway's specific coverage details, as deductibles and coinsurance payments are usually involved. These costs can vary depending on the length of stay and the specific services received.

- Deductibles: Mrs. Ridgeway will likely face a deductible for each "benefit period" of hospital care. A benefit period begins when she is admitted to a hospital and ends when she has been out of the hospital for 60 consecutive days.

- Coinsurance: After the deductible is met, Part A may cover a percentage of the costs, with Mrs. Ridgeway responsible for the remaining coinsurance.

- Skilled Nursing Facility Care: Part A also helps cover short-term rehabilitation care in a skilled nursing facility, but it’s usually limited to a specific duration and requires a qualifying hospital stay.

Understanding the limitations of Part A is vital: It doesn't cover everything. For instance, long-term care in a nursing home is generally not covered by Part A. Mrs. Ridgeway needs to be aware of this potential out-of-pocket expense.

Part B: Medical Insurance

Part B covers a broader range of medical services than Part A, including doctor visits, outpatient care, preventive services, and some home healthcare. Unlike Part A, Part B typically requires a monthly premium. The premium amount depends on Mrs. Ridgeway's income. Higher earners pay more.

- Premium Costs: The monthly premium amount for Part B is determined by the Social Security Administration based on her modified adjusted gross income (MAGI) from two years prior. This means that Mrs. Ridgeway's premium may change annually based on her income.

- Annual Deductible: Part B has an annual deductible that Mrs. Ridgeway is responsible for paying before Medicare begins to cover her expenses.

- Coinsurance and Copayments: After meeting the deductible, Medicare typically covers 80% of the approved amount for most services, leaving Mrs. Ridgeway responsible for the remaining 20% coinsurance. Some services may also have copayments.

Gaps in Original Medicare Coverage: The Need for Supplemental Insurance

Original Medicare, while providing significant coverage, leaves gaps that can lead to substantial out-of-pocket expenses for Mrs. Ridgeway. These gaps include:

- Part B coinsurance: The 20% coinsurance can add up quickly, especially for those with multiple medical needs.

- Part A coinsurance: While Part A covers a substantial portion of hospital stays, the coinsurance for longer stays can be significant.

- Medically necessary services that Medicare doesn't cover: Certain services, even if medically necessary, might not be covered by Original Medicare.

- Prescription drug coverage: Original Medicare does not include prescription drug coverage.

Because of these gaps, many beneficiaries, including Mrs. Ridgeway, consider supplemental insurance options to help manage these costs.

Medigap (Medicare Supplement Insurance): Bridging the Gaps

Medigap plans, also known as Medicare Supplement Insurance, are offered by private insurance companies and are designed to help pay for some of the healthcare costs that Original Medicare doesn't cover. These plans are standardized, meaning that a Medigap Plan G in one company will offer essentially the same coverage as a Medigap Plan G in another company. Choosing the right Medigap plan is crucial for Mrs. Ridgeway's financial protection.

Several Medigap plans exist, each offering a different level of coverage. Some popular plans include:

- Plan G: This plan is very popular because it covers the Part B deductible and the Part B coinsurance. It also pays for the Part A coinsurance and hospital costs.

- Plan F: Similar to Plan G, but also covers the Part B deductible. Note that Plan F is no longer available to new Medicare beneficiaries.

- Plan N: This plan has a lower premium than Plan G, but it has co-payments for some doctor visits and outpatient care.

It's essential for Mrs. Ridgeway to carefully compare different Medigap plans based on her individual needs and budget before making a decision. Factors to consider include:

- Premium costs: The monthly premiums vary between plans.

- Coverage levels: Some plans offer more comprehensive coverage than others.

- Financial stability of the insurance company: It’s vital to choose a financially sound insurer.

Part D: Prescription Drug Coverage

Original Medicare doesn't include prescription drug coverage. To obtain prescription drug coverage, Mrs. Ridgeway needs to enroll in a separate Medicare Part D plan, offered by private insurance companies. These plans work similarly to Medigap, offering different levels of coverage with varying premiums and formularies (lists of covered drugs).

- Selecting a Part D plan: Mrs. Ridgeway needs to carefully review the formulary to ensure her prescription medications are covered. This is critical to manage her out-of-pocket costs.

- Premium Costs and Deductibles: Part D plans have premiums, deductibles, and cost-sharing that vary among plans and based on the prescription drugs needed.

- Late Enrollment Penalties: Delaying Part D enrollment may result in penalties, increasing monthly premiums.

Navigating the Medicare Maze: Tips for Mrs. Ridgeway

Enrolling in Medicare can be confusing, even for those familiar with the healthcare system. Here are some helpful tips for Mrs. Ridgeway:

- Attend Medicare counseling sessions: These sessions offer personalized guidance and help navigate the complexities of Medicare enrollment and coverage.

- Compare plans carefully: Use Medicare's online tools and resources to compare different Medigap and Part D plans.

- Contact Medicare directly: If she has any questions or concerns, Mrs. Ridgeway should contact Medicare directly for clarification.

- Consult a financial advisor: A financial advisor specializing in Medicare can provide expert guidance on choosing the best coverage options.

- Review your coverage annually: Medicare benefits and costs can change annually, making it important to review her coverage and potentially adjust her plan as needed.

The Importance of Proactive Planning

Understanding and enrolling in the appropriate Medicare plans is crucial for Mrs. Ridgeway's financial well-being and access to healthcare. Proactive planning, including careful review of coverage options, comparison shopping, and understanding the limitations of Original Medicare, will help her make informed decisions and avoid costly surprises. By diligently researching and seeking expert advice when needed, she can ensure that she has the best Medicare coverage to meet her healthcare needs.

Conclusion: Securing Mrs. Ridgeway's Healthcare Future

This comprehensive guide aimed to illuminate the intricacies of Mrs. Ridgeway's enrollment in Original Medicare. By understanding Parts A and B, the need for supplemental coverage (Medigap), and the importance of prescription drug coverage (Part D), she can confidently navigate the Medicare system. Remembering that proactive planning and regular review of her coverage are key to maintaining optimal healthcare access and financial stability in her retirement. This will ensure she receives the best possible care while mitigating unexpected out-of-pocket expenses. Seeking assistance from Medicare counselors or financial advisors can significantly simplify the process and offer peace of mind.

Latest Posts

Latest Posts

-

You Should End Business Phone Calls

Mar 13, 2025

-

Chapter Summary Of Dr Jekyll And Mr Hyde

Mar 13, 2025

-

Hesi Case Studies Heart Failure With Atrial Fibrillation

Mar 13, 2025

-

4 04 Quiz Buying Clothes And Shopping 2

Mar 13, 2025

-

Traffic School Questions And Answers Pdf

Mar 13, 2025

Related Post

Thank you for visiting our website which covers about Mrs Ridgeway Enrolled In Original Medicare . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.