When A Corporation Pays A Note Payable And Interest

Onlines

Apr 03, 2025 · 6 min read

Table of Contents

When a Corporation Pays a Note Payable and Interest: A Comprehensive Guide

Paying off a note payable, including the principal and accrued interest, is a crucial aspect of corporate finance. Understanding the accounting implications, the different methods of repayment, and the potential tax consequences is vital for maintaining sound financial health. This comprehensive guide delves into the intricacies of note payable payments, offering a detailed explanation for business owners, accountants, and anyone interested in corporate finance.

What is a Note Payable?

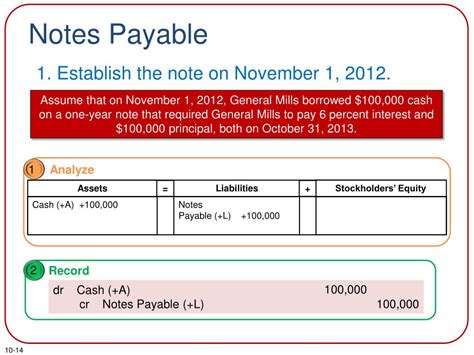

A note payable is a formal written promise to repay a debt. It's a liability recorded on a company's balance sheet, representing a short-term or long-term obligation to pay a specific amount of money on a predetermined date or dates. These notes typically include details such as:

- Principal Amount: The original amount borrowed.

- Interest Rate: The percentage charged on the principal amount.

- Maturity Date: The date on which the principal and interest are due.

- Payment Terms: Specifies how and when payments will be made (e.g., monthly installments, single lump sum).

Corporations use notes payable for various purposes, including:

- Short-term financing: Bridging temporary cash flow gaps.

- Long-term financing: Funding major capital expenditures or acquisitions.

- Supplier financing: Obtaining credit from suppliers to purchase goods or services.

- Bank loans: Securing financing from financial institutions.

Accounting for Note Payable Payments

The accounting treatment of note payable payments depends on whether the payment is made at maturity or through installments.

Single Payment at Maturity

When a note payable is paid in a single lump sum at maturity, the journal entry involves debiting the Note Payable account and crediting the Cash account. The total amount debited will include the principal amount plus any accrued interest.

Example:

Let's assume a corporation borrowed $10,000 with an annual interest rate of 5% for one year. At maturity, the corporation needs to pay the principal plus the interest.

- Interest accrued: $10,000 * 0.05 = $500

- Total payment: $10,000 + $500 = $10,500

The journal entry would be:

| Account Name | Debit | Credit |

|---|---|---|

| Note Payable | $10,000 | |

| Interest Expense | $500 | |

| Cash | $10,500 |

Installment Payments

When a note payable is repaid in installments, each payment typically includes a portion of the principal and interest. The allocation of each payment between principal and interest is determined using an amortization schedule. This schedule details the principal and interest components of each payment over the life of the loan.

Example:

Consider a $10,000 loan with a 5% annual interest rate and a 2-year term, paid in equal monthly installments. The amortization schedule will calculate the monthly payment amount and distribute it between principal and interest reduction for each month. Each month, the interest expense will be calculated on the outstanding principal balance. The journal entry for each payment would be:

| Account Name | Debit | Credit |

|---|---|---|

| Note Payable | $XXX | |

| Interest Expense | $YYY | |

| Cash | $ZZZ |

Where:

- $XXX is the portion of the payment applied towards the principal.

- $YYY is the interest expense for that payment period.

- $ZZZ is the total monthly payment.

Determining Interest Expense

Accurately calculating interest expense is critical. The interest expense is typically calculated using the following formula:

Interest Expense = Principal Balance * Interest Rate * Time

Where:

- Principal Balance: The outstanding principal amount of the loan. This decreases with each payment for installment loans.

- Interest Rate: The annual interest rate, expressed as a decimal.

- Time: The fraction of the year that the interest applies to. For example, if the interest is calculated monthly, the time would be 1/12.

Tax Implications of Note Payable Payments

Interest expense paid on notes payable is generally tax-deductible. This deduction reduces the corporation's taxable income, lowering its overall tax liability. However, it's crucial to adhere to tax laws and regulations specific to the relevant jurisdiction. Certain restrictions might apply, depending on the nature of the loan and its use. Consult with a tax professional for accurate and up-to-date tax advice.

Different Types of Notes Payable

Several types of notes payable exist, each with unique characteristics:

- Short-term notes payable: Mature in less than one year. They are often used for short-term financing needs.

- Long-term notes payable: Mature in over one year. They are frequently used for significant capital investments.

- Secured notes payable: Backed by collateral, offering lenders a degree of protection in case of default.

- Unsecured notes payable: Not backed by collateral, relying on the borrower's creditworthiness.

- Interest-bearing notes payable: Accrue interest over the loan term.

- Non-interest-bearing notes payable: Do not explicitly accrue interest; however, the interest might be implicitly incorporated into the principal amount.

Early Payment of Notes Payable

Sometimes, corporations may have the opportunity or the need to pay off a note payable earlier than its maturity date. This often involves a prepayment penalty, a fee charged by the lender for breaking the loan agreement early. The exact amount of the prepayment penalty will depend on the terms specified in the note payable agreement. The accounting treatment would involve recording the prepayment penalty as an expense.

Importance of Accurate Record Keeping

Maintaining accurate records of all note payable transactions is paramount. This includes meticulously tracking all payments, interest accrued, outstanding principal balances, and any associated fees. Accurate record-keeping is crucial for:

- Financial Reporting: Ensuring the accurate presentation of financial statements.

- Tax Compliance: Supporting tax filings and minimizing potential tax liabilities.

- Internal Control: Enhancing the efficiency and integrity of financial operations.

- Creditworthiness: Demonstrating responsible financial management to potential lenders and investors.

Potential Issues and Risks

Several potential issues and risks are associated with note payable management:

- Default: Failure to make payments as agreed upon can lead to severe financial consequences, including legal action and damage to creditworthiness.

- High Interest Rates: Borrowing at excessively high interest rates can significantly strain a company's finances.

- Restrictive Covenants: Loan agreements may include covenants that limit a company's operating flexibility.

- Cash Flow Management: Inadequate cash flow management can lead to difficulties in meeting payment obligations.

Conclusion

Understanding the intricacies of note payable payments is fundamental to sound corporate financial management. From the accounting implications and the various types of notes payable to the tax consequences and potential risks, a thorough grasp of these concepts is crucial for maintaining a healthy financial position. Proactive planning, accurate record-keeping, and seeking professional advice when necessary are key to effectively managing notes payable and ensuring long-term financial success. By diligently addressing these aspects, corporations can leverage debt financing to fuel growth while mitigating potential risks. Remember, responsible debt management is a cornerstone of sustainable business growth.

Latest Posts

Latest Posts

-

Which Role Does Product Management Work With To Prioritize Enablers

Apr 04, 2025

-

Review Sheet 13 Neuron Anatomy And Physiology

Apr 04, 2025

-

7 2 10 Configure Management Vlan Settings Cli

Apr 04, 2025

-

3 3 6 Endangered Animals Add Color Coding

Apr 04, 2025

-

Autumns School Holds A Volunteer Challenge

Apr 04, 2025

Related Post

Thank you for visiting our website which covers about When A Corporation Pays A Note Payable And Interest . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.